קורס בינה מלאכותית : RB20 – שיעור 3 Time series ולמידת מכונה

יצירת VIRTUAL ENV

הרצת ה ENV

conda create –name env_image1 python=3.5.4

conda activate env_image1

conda info –envs

למשל

D:\TWS API\source\pythonclient

הסדרות אינם מציטות ל GUASS-MRKOV בניגוד למידע ריגרסיה ליניארי

index2018.csv ייש להורדי

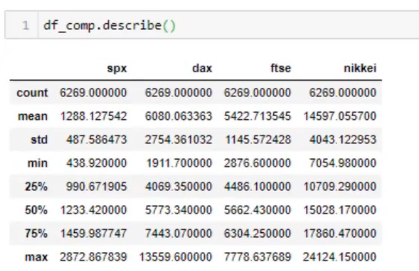

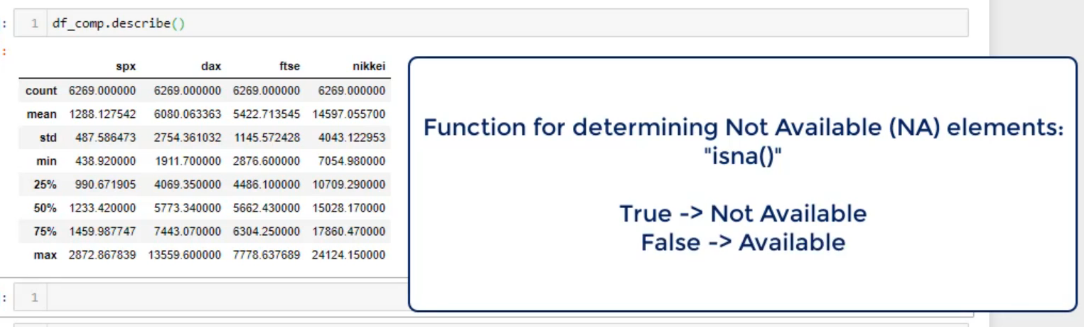

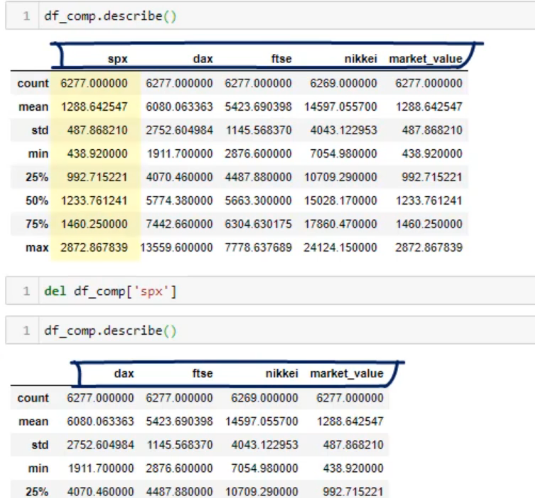

נבדוק בצורה ראשונית את הנתונים

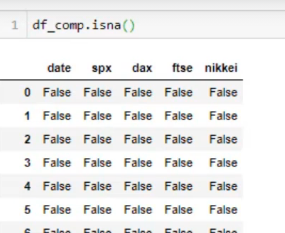

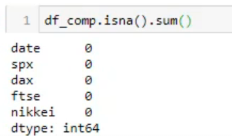

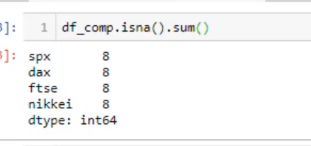

נריץ בדיקה איפה חסר נתונים :

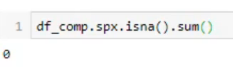

פניה ישירה לעמודה

הדפסת הערכים

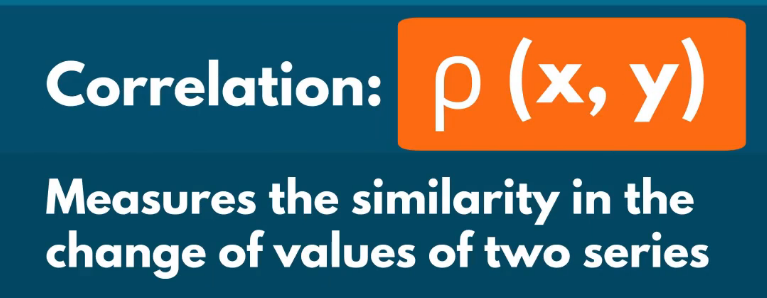

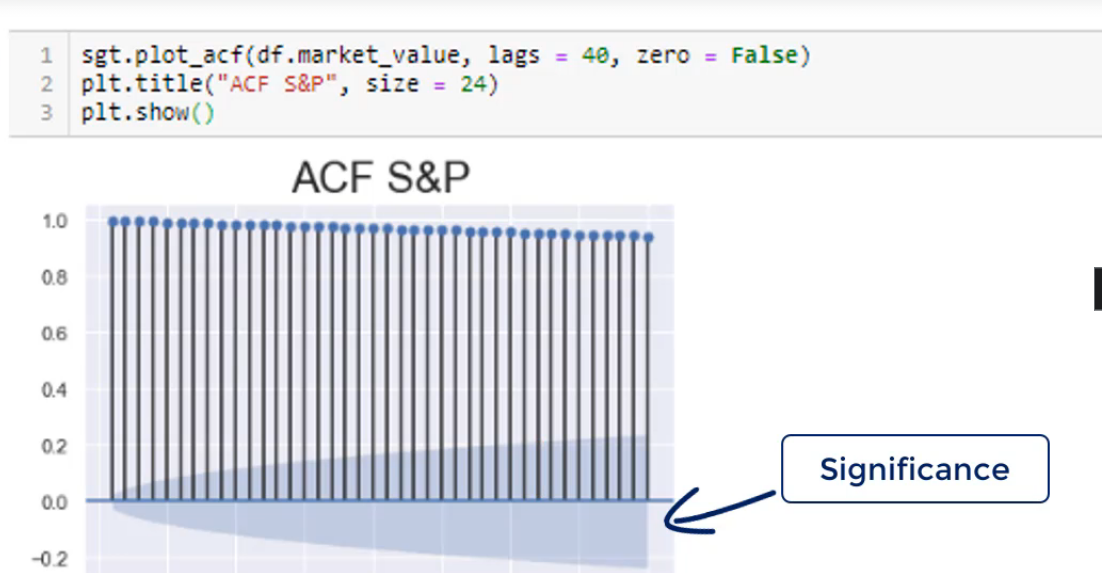

קרולציות בין שתי סדרות זמן

QQ PLOT

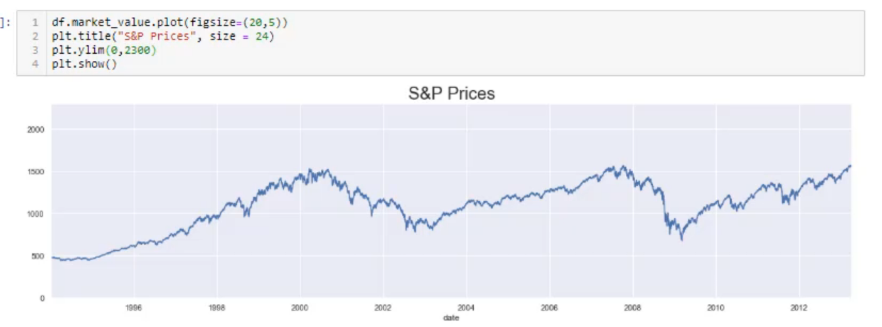

ציך ה Y מראה ערך למשל מחיר מ 0 עד 3000

ציר ה X מראה את כמות הפיזור – יש לבדוק לעומק התפלגות זאת

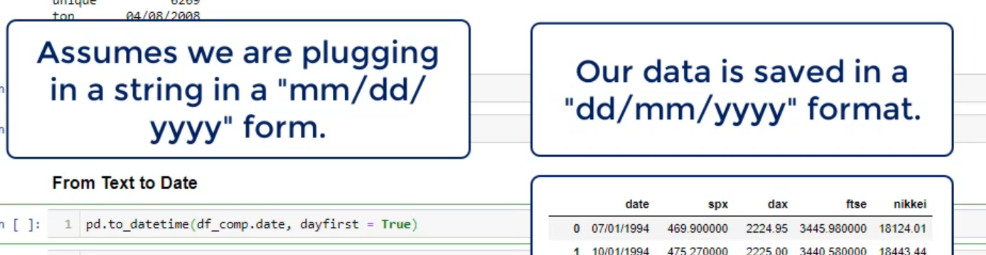

DATE

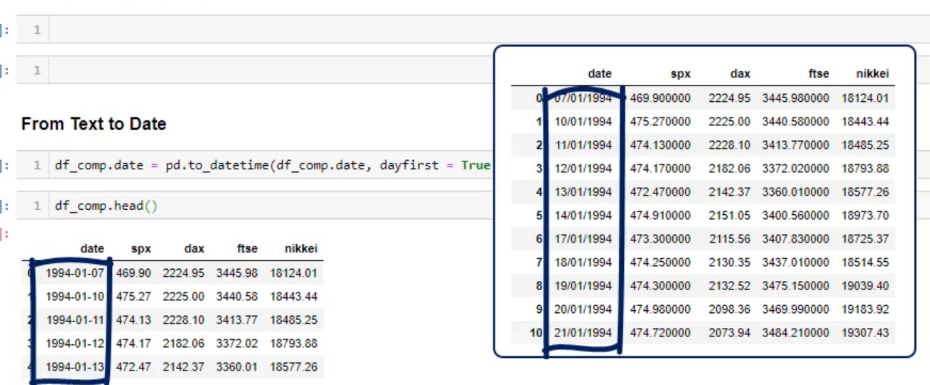

נמיר את הזמן מצב טקסט למצב תאריך

נכניס לתוך משתנה

עכשיו נקבל מידע בצורה טובה – שנוכל לבצע ניתוח

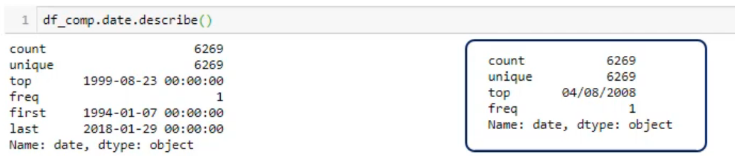

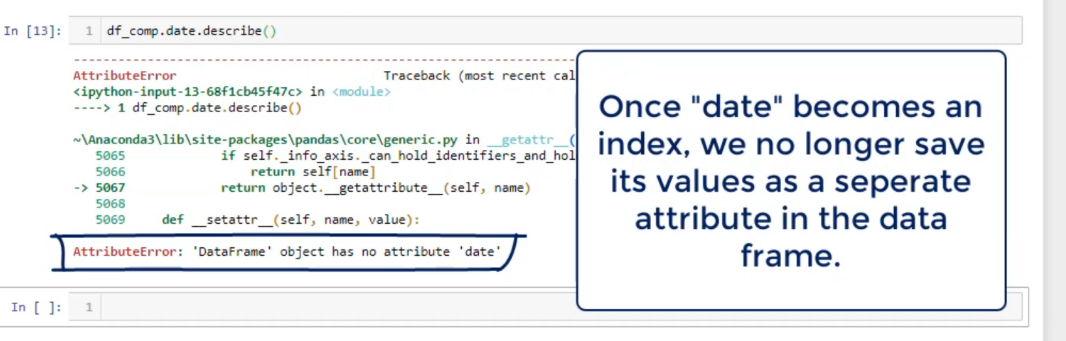

יצרית אינדקס DATE

בגלל שהם אינדקס

re kph hnh gcsuv

ממלאים תאים חסרים לפי תא לפני או תא אחרי ועוד

פיצול דאטא פריים עבור למידת מכונה

![]()

בדיקה שאין OVER LAPPING

ניצור רעש לבן על DATAFRAME קיים

![]()

על מנת להשוות סדרות צריך שיהיה להם אותו אורך ואותו גובה

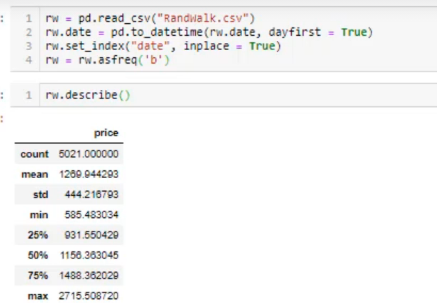

רעש לבן

,

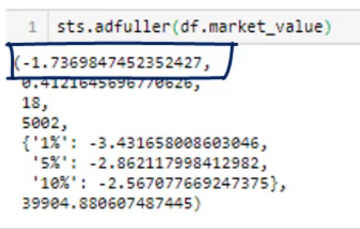

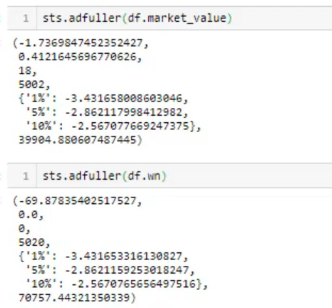

Stationarity

here are some examples of stationary and non-stationary time series:

- Stationary Time Series:

An example of a stationary time series is a series of annual rainfall measurements over many years in a region where the climate remains relatively constant. In this case, the mean, variance, and autocovariance of the rainfall measurements remain constant over time.

- Non-Stationary Time Series:

An example of a non-stationary time series is a series of monthly temperature measurements over many years in a region that experiences seasonal changes. In this case, the mean temperature, variance, and autocovariance of the temperature measurements change over time due to seasonal fluctuations.

Another example of a non-stationary time series is a stock price series that shows an increasing or decreasing trend over time. In this case, the mean of the series is changing over time, which violates the stationarity assumption.

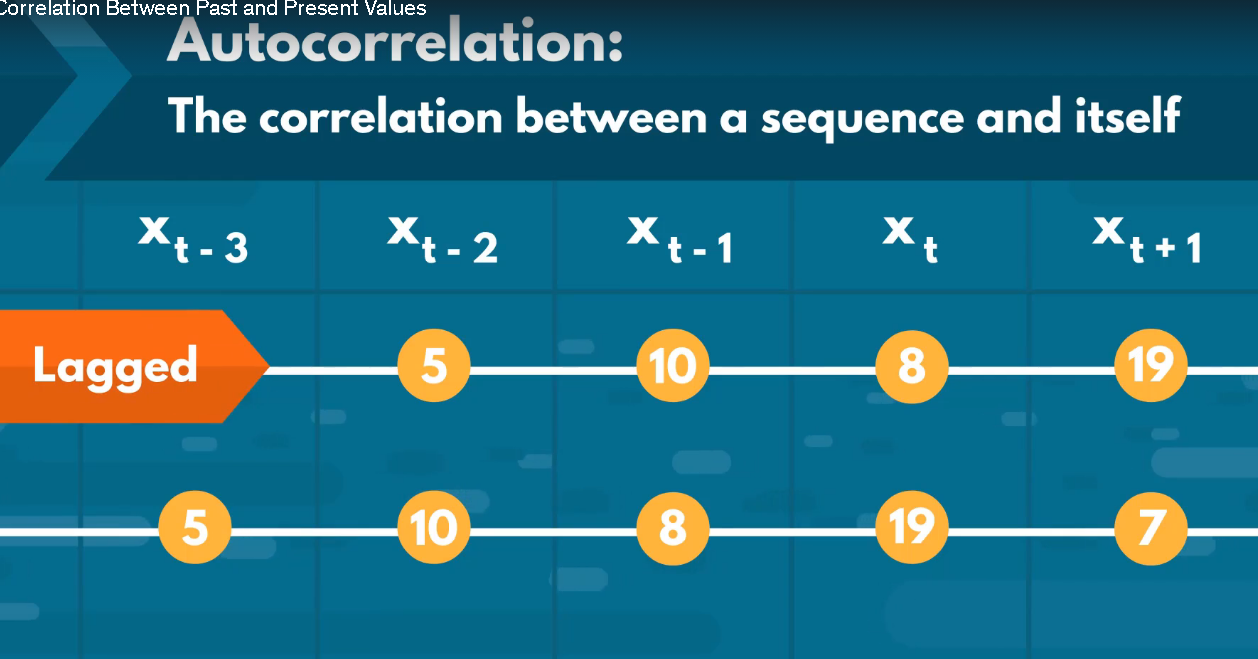

ACF- Autocorrelation

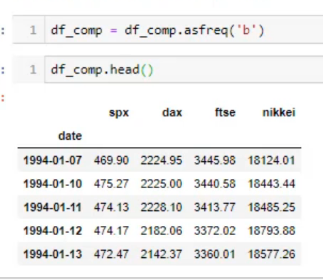

20. Setting the Frequency